Investment Highlights from Charles A. Kennedy, Chief Investment Officer

Overview

Created through generous gifts and augmented by careful financial stewardship, Carnegie Mellon University’s endowment stood at a market value of $3.1 billion as of June 30, 2021. The endowment serves as a key strategic asset of the university. Carnegie Mellon seeks to advance knowledge and understanding in science and technology, fine arts and the humanities through its research and education mission.

By providing a permanent and consistent source of funding for scholarships, professors’ salaries, laboratory equipment and other important needs, the endowment enables our faculty and students to carry out the university’s mission. Critically, endowment support for tuition assistance attracts and retains a highly qualified and diverse student body. With its perpetual life, the endowment is uniquely situated to provide funding today, tomorrow and for future generations to advance the university’s mission and to help our students and faculty achieve their goals and aspirations.

Strategy and Allocation

The endowment’s portfolio of investments is managed with a long-term, growth-oriented view and evaluated by its effectiveness in achieving — over time — two fundamental objectives: (1) generating steady and substantial financial support for students, faculty and programs; and (2) balancing current demands for support with the goal (at a minimum) of maintaining the endowment’s real purchasing power for future generations (i.e., preserving intergenerational equity). To maximize long-term expected returns within acceptable levels of risk and liquidity, Carnegie Mellon designed its policy asset allocation using a combination of academic theory, quantitative analysis and informed market judgment.

To achieve the objectives stated above, Carnegie Mellon targets broad portfolio exposure of 85% in equity investments for long-term growth and appreciation, and 15% in fixed income investments to provide stability and liquidity. Fiscal year 2021 (FY21) marks the 17th anniversary of the university’s decision to shift the equities focus from traditional, publicly traded investments to private investments, primarily utilizing private equity funds globally. We believe that over the long term, private equity investment returns, including those from emerging markets funds, will exceed the returns generated from investing in public securities.

Environmental, social and governance (ESG) issues can affect the performance of investment portfolios (to varying degrees across companies, sectors, regions, regulatory regimes, asset classes and through time). Attention to ESG issues by investors and company management teams encourages accountability, transparency, sustainability and ethical behavior in business practices, which may lead to reduced exposure to various risks and improved long-term value creation. Importantly, the university does not pursue ESG investing as a strategy distinct from its central investing focus. Carnegie Mellon integrates ESG factors into its multifaceted investment analyses and we expect our investment managers to do the same. Monitoring our managers’ incorporation of ESG initiatives into their value creation strategies gives us insight into their ability to persistently increase value in their operating companies, which benefits us all.

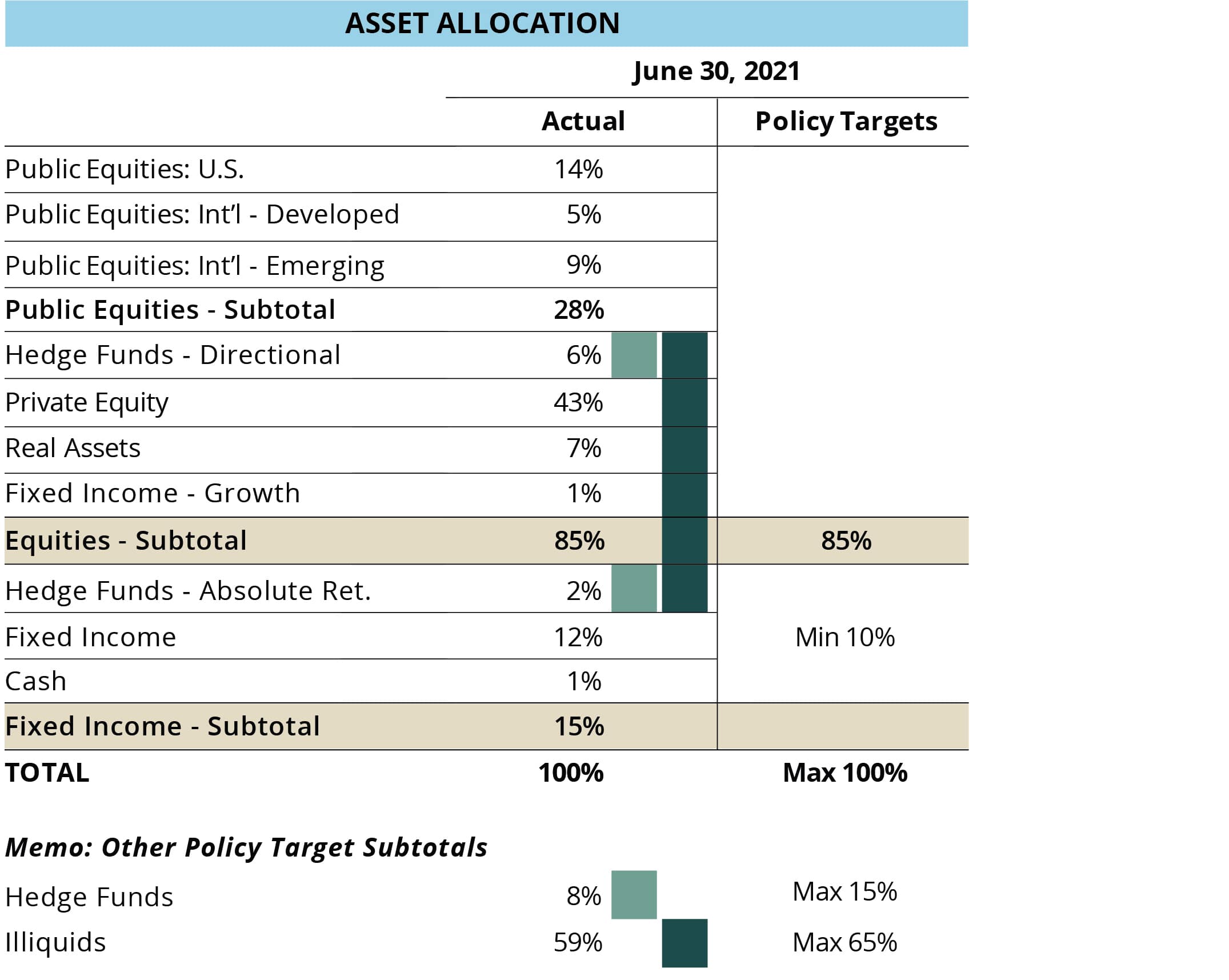

Given return dispersions that can persist for extended periods of time across traditional asset class categories, Carnegie Mellon updated its asset allocation model during FY21 to allow more flexibility to concentrate capital with managers pursuing themes and strategies with multigenerational return potential while maintaining ample portfolio liquidity. Figure 1 details asset allocation targets and actual allocations as of June 30, 2021.

Figure 1: Asset Allocation — Actual Allocations and Policy Target

As depicted in Figure 1, the endowment is at its 85% equities target and well within other policy constraints. At this 17th anniversary of the pursuit of the university’s long-term strategy, Carnegie Mellon’s private portfolio is maturing. However, the nature of private equity investing and the growth of Carnegie Mellon’s endowment necessitate a continuing focus on expanding our best private equity relationships and identifying the next generation of top tier managers. Fortunately, Carnegie Mellon’s endowment is of a size that permits new, reasonably sized commitments to value-creating investment managers that will be meaningful to the endowment’s asset allocation and investment return.

Investment Performance

The university’s net investment return for FY21 was 42.6%. More significantly, given the long-term goals of the investment strategy and the “noise” (versus signal) often associated with short-term equity results, Carnegie Mellon’s three-, five- and 10-year returns were 17.5%, 15.4% and 10.9%, respectively. These returns compare favorably with relevant benchmarks.

Endowment Attribution

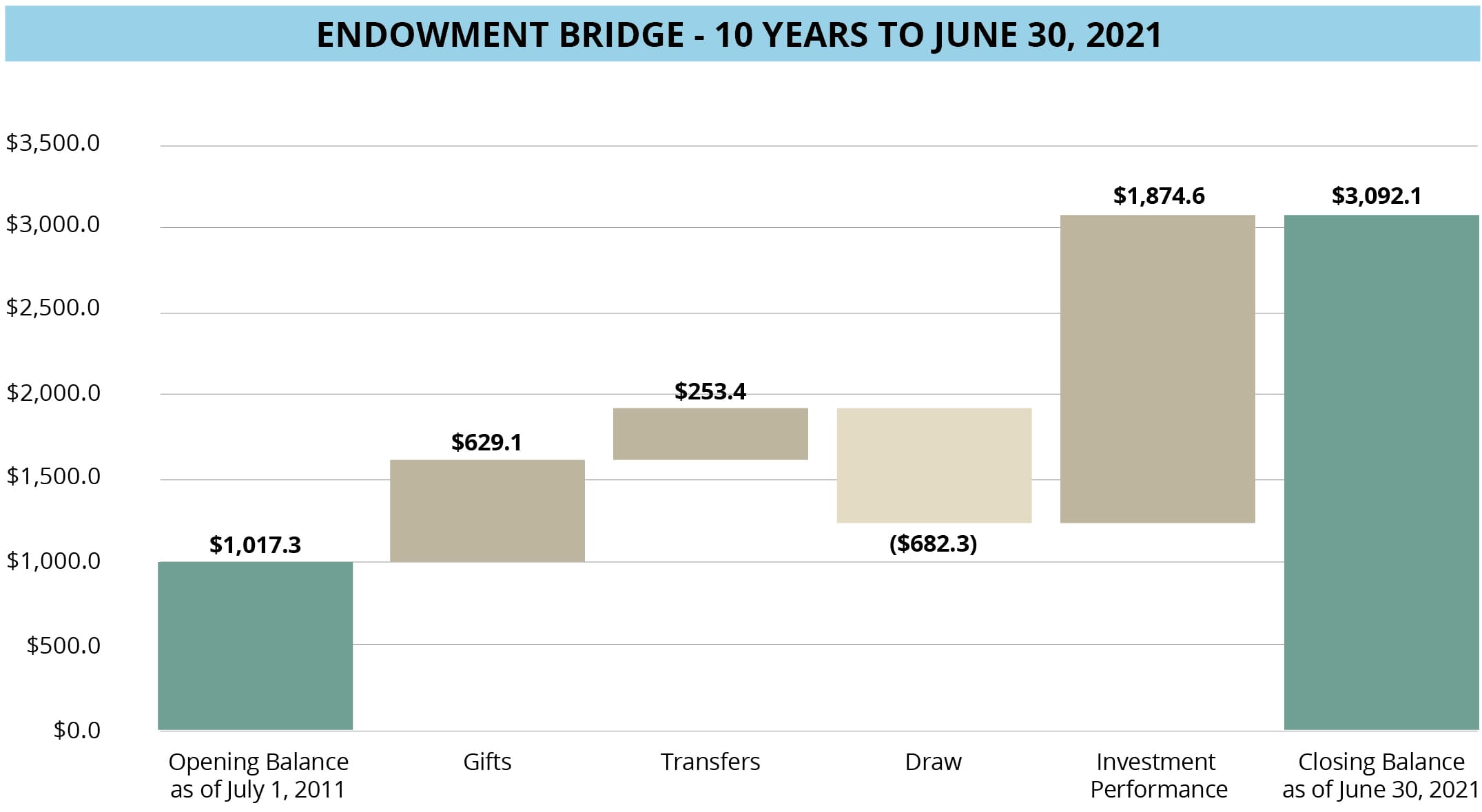

The endowment’s market value increased to $3,092.1 million as of June 30, 2021, from $2,068.9 million as of June 30, 2020. This net increase of approximately $1,023.2 million reflects the collective impact of $217.2 million from gifts and other sources, plus $906.4 million from investment gains, less $100.4 million of distributions to support the university’s operations. As depicted in Figure 2, for the 10-year period ended June 30, 2021, the endowment’s market value increased approximately $2,074.8 million (from a beginning market value of $1,017.3 million), reflecting the collective impact of $882.5 million from gifts and other sources, plus $1,874.6 million from investment gains, less $682.3 million of distributions to support the university’s operations.

Figure 2: Endowment Bridge

(dollars in millions)

As previously noted, cash distributions from the endowment (i.e., the draw) provide a key source of support for various university activities and programs in need of consistent funding ranging from general operations to scholarships and professorships. During the last decade, the draw from the endowment has grown from supporting less than 5% of the university’s operations to 8% for FY21. Overall, the draw grew both in absolute terms and relative to the operating budget of the university (which grew 3.1% annually over the decade), while following a consistent draw policy (see Note 7 on p. 22 of the consolidated financial statements). Even with the higher level of support, the university’s endowment contributes only about one-third of the relative operating support received by many academic peers from their endowments. This variance leaves Carnegie Mellon more dependent on tuition and sponsored research than its peers. Consequently, Carnegie Mellon remains focused on growing the endowment to assure the financial resources and flexibility exist to successfully pursue its long-term research and education mission.

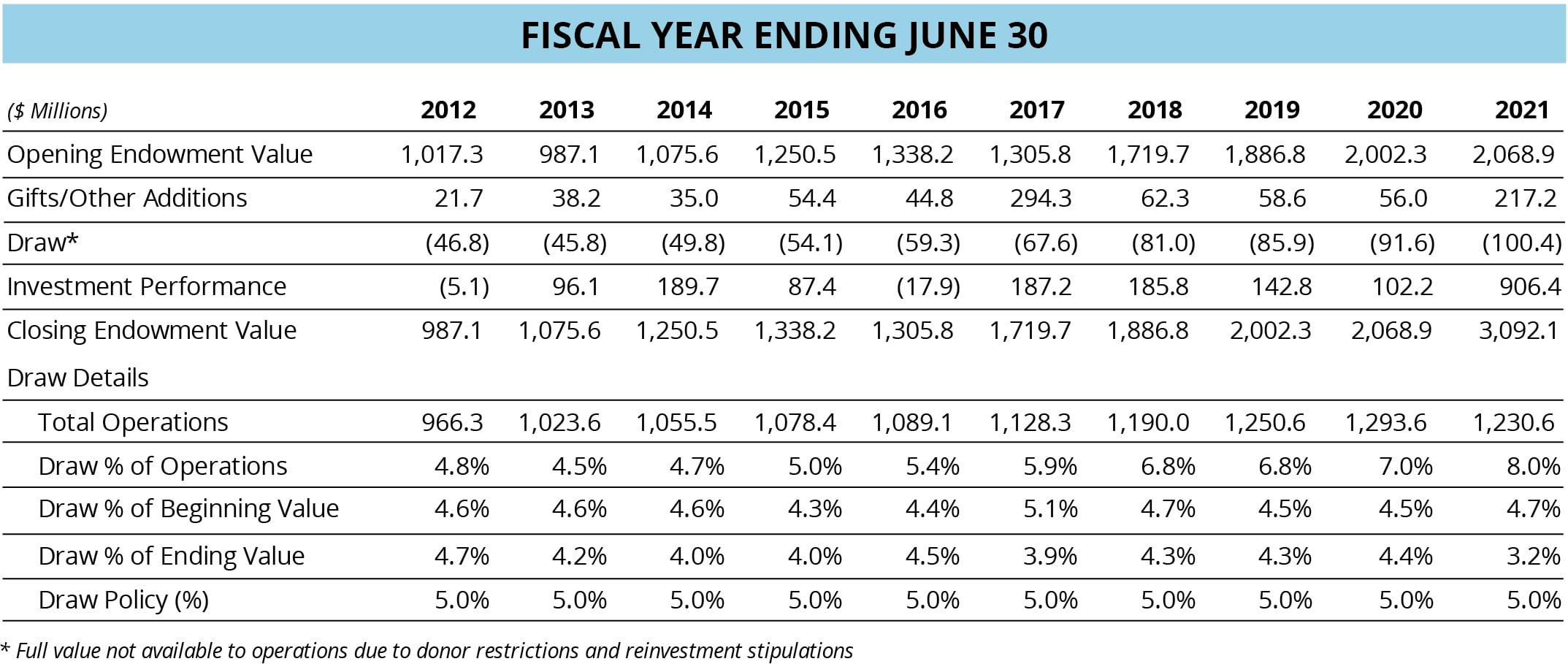

The historical activities of the endowment, including the draw and its support expressed as a percentage of annual operations, are summarized in Figure 3.

Figure 3: Endowment Values and Attribution

The Dietrich Foundation

The Dietrich Foundation, established by Pittsburgh industrialist and longtime university trustee William S. Dietrich II, was created to manage in perpetuity his gift of approximately $500 million in assets intended to benefit the university and other higher education and charitable institutions. The Dietrich Foundation’s assets are not reflected in the university’s financial statements (see additional information regarding the foundation in Note 17 on p. 37 of the consolidated financial statements). The university’s share of the annual distributions from The Dietrich Foundation is 53.5%. If this percentage is applied to the estimated value of The Dietrich Foundation’s assets of $1,636 million as of June 30, 2021, and the result added to Carnegie Mellon’s endowment of $3,092.1 million, the combination would total $3,967.4 million. Annual distributions from The Dietrich Foundation over time equal 3% of the value of the foundation’s net assets as measured on January 1 of each year. The Dietrich Foundation’s gift added to Carnegie Mellon’s endowment for FY21 was $17.3 million, and cumulative gifts since the initial gift in FY13 total $111.4 million.

Summary

Carnegie Mellon’s endowment provides an important and permanent source of financial and operational stability, which helps university leadership to perpetuate academic and research excellence in a rapidly changing and increasingly competitive world. Enduring generosity of alumni and friends and an investment program focused on compounding net returns for the long term should continue to increase the value of Carnegie Mellon’s endowment over time, providing ongoing support for the university’s operating needs while preserving purchasing power to support future generations of students, faculty and programs.

Sincerely,

Charles A. Kennedy

Chief Investment Officer

November 5, 2021