Investment Highlights from Charles A. Kennedy, Chief Investment Officer

Strategy and Allocation

Carnegie Mellon University’s endowments were gifted to the university to serve as a key contributor to the institution’s long-term mission. Providing a permanent and consistent source of funding, the endowments enable Carnegie Mellon to pursue research and education initiatives, including sponsoring student scholarships, that would not otherwise be available. Consequently, keen university stewardship of these funds is essential.

In fiscal year 2017, CMU's endowments (or collectively endowment) supported 6.0 percent of university operations. This percentage is only about one-third that of other universities with endowments greater than $1 billion. The university’s endowment contribution to operations is relatively even smaller when compared to a smaller group of peer institutions. This situation leaves Carnegie Mellon more dependent on tuition and sponsored research than its peers, thereby reducing its financial flexibility. This shortfall is being addressed through a greater focus on building the endowments for the university over the long-term. Fiscal year 2017 marks the fifth consecutive year where endowment support as a percentage of the operating budget has increased, starting with 4.5 percent of the university’s operations in fiscal year 2013. This relatively higher support has been achieved while the overall university’s operations have continued to grow.

Endowments provide a perpetual source of financial and operational stability in a constantly changing environment, which allows the university leadership to perpetuate CMU’s academic and research excellence in an increasingly competitive world.

Accordingly, the endowment portfolio is managed with a long-term, growth-oriented view and evaluated by its effectiveness in achieving, over time, two fundamental objectives: (1) generating steady and substantial financial support for Carnegie Mellon students, faculty and programs; and (2) balancing the current needs of our various constituencies with the goal of maintaining the endowment's real purchasing power for future generations (i.e., preserving "intergenerational equity").

In order to maximize long-term expected returns within acceptable levels of risk and liquidity, Carnegie Mellon designed its policy asset allocation to use a combination of academic theory, quantitative analysis and informed market judgment.

Fiscal year 2017 marks the 13th anniversary of the university’s decision to better position the portfolio to achieve its long-term performance goals by shifting the focus of the portfolio from traditional, publicly traded investments to private investments, including some within rapidly growing international markets. Investing through private equity funds encompasses a lengthy process of selecting allocation targets for various asset classes (e.g., venture capital, buyouts and real assets), evaluating and selecting fund managers, and ultimately making commitments to long-term private partnerships as fund managers come to market periodically. After a commitment to a fund is made, investors are then called upon to provide capital as the fund managers discover, acquire and invest in companies during an investment period that generally lasts several years. After fund investments are made, the fund manager, whose own interests are generally well-aligned with fund investors, will seek to add value to the underlying company in several ways, including increasing sales and profitability, improving capital management and otherwise improving long-term prospects so that the business can be sold for more than its purchase price.

While these acquisition, value-add and harvesting processes may take several years each, we believe that, over the long-term, talented fund managers will be able to exceed the return available from investing in public securities, thereby enabling the endowments to better contribute to the university's mission. The typical private partnership is created for 10 years in order for the above-mentioned processes to take place. As described, investing in private funds is a lengthy process that takes several years to achieve a target allocation with a mature underlying portfolio of companies. At this 13th anniversary of the university's commitment to the new strategy, CMU's private portfolio is maturing. However, recent contributions to the endowments have resulted in below targeted private investment allocations. Achieving the target will require several years of commitments, capital calls and the maturing of underlying investments.

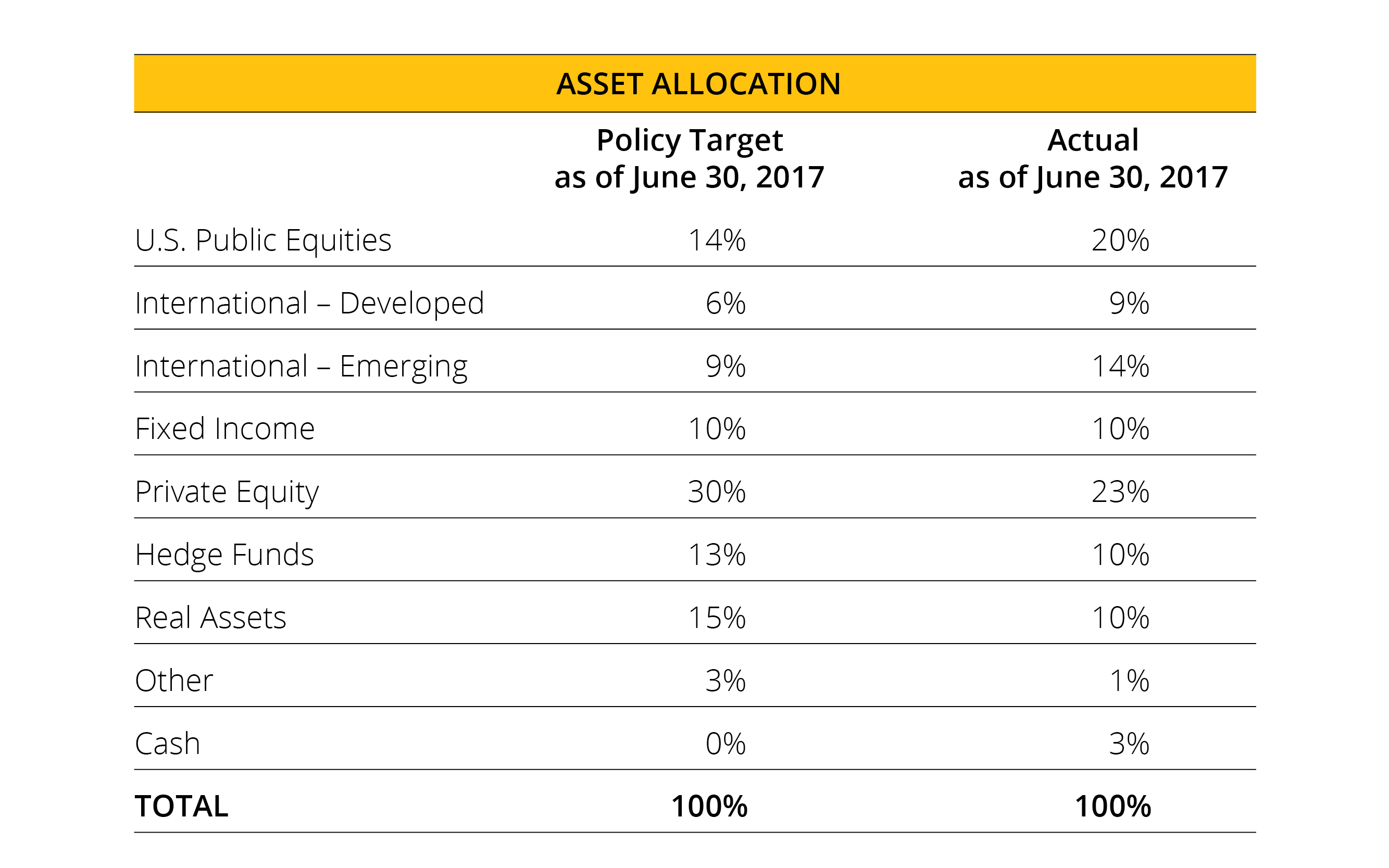

The following table details the asset allocation targets and the actual allocation as of June 30, 2017:

Figure 1 – Policy Allocation Targets and June 30, 2017 Allocations

The 14 percentage point over-allocation (compared to target) to U.S. and international public equities was offset by an equal under-allocation to private investments in private equity and real assets. This over-allocation was primarily due to a large cash influx to the endowment from the university in fiscal year 2017. During the prior fiscal year, the university received proceeds from a large lawsuit settlement. The board of trustees concurred with the recommendation of the university president and an ad hoc committee — comprising the university provost, the dean of the College of Engineering and a member of the board — to move the bulk of the university’s share of the proceeds into the endowment. A board resolution was passed in October 2016 instructing that $200 million of the lawsuit settlement proceeds be moved into the endowment. Later in the fiscal year, the university moved another $16 million into the endowment for a total $216 million.

Investment Performance

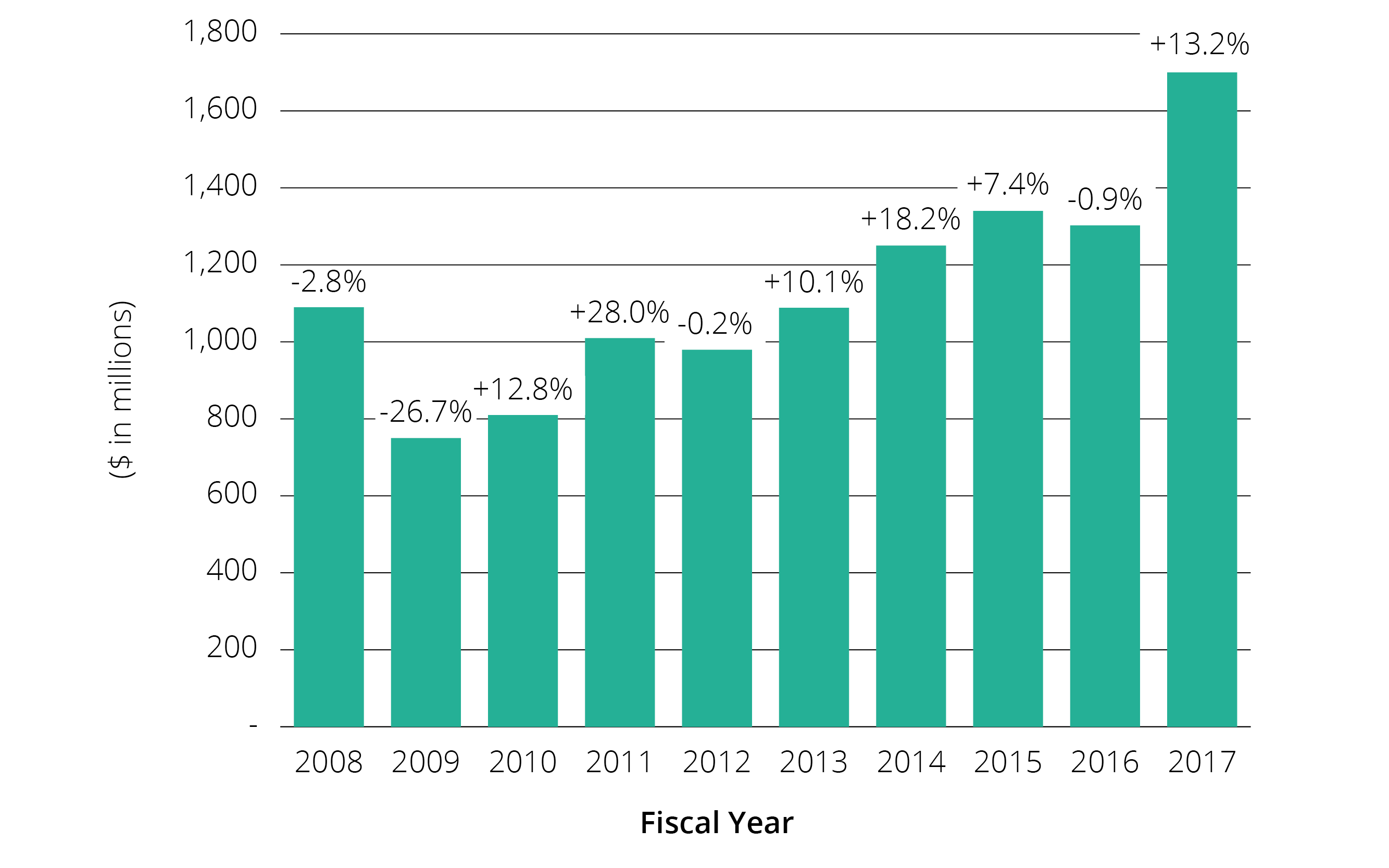

The university’s investment performance for fiscal year 2017 was 13.2%.

More significantly given the long-term goals of the investment strategy, Carnegie Mellon's three- and five- year returns were 6.4 percent and 9.4 percent. The university's one-year return followed a return of -0.9 percent for fiscal year 2016 and 7.4 percent for fiscal year 2015. (Note: Some institutions report results on a lagged basis reflecting a lag of one quarter for private investment funds. When incorporating this lag into the return for fiscal years 2017, 2016 and 2015, the university returns would have been 13.0 percent, -0.1 percent, and 7.1 percent, respectively.)

Acknowledging that investment returns are inherently difficult to predict, the continued low interest rate environment relative to historical rates and other changes in the market may lead to lower returns in the future.

Figure 2 – Endowment Ending Value and Annual Investment Return

Endowment Attribution

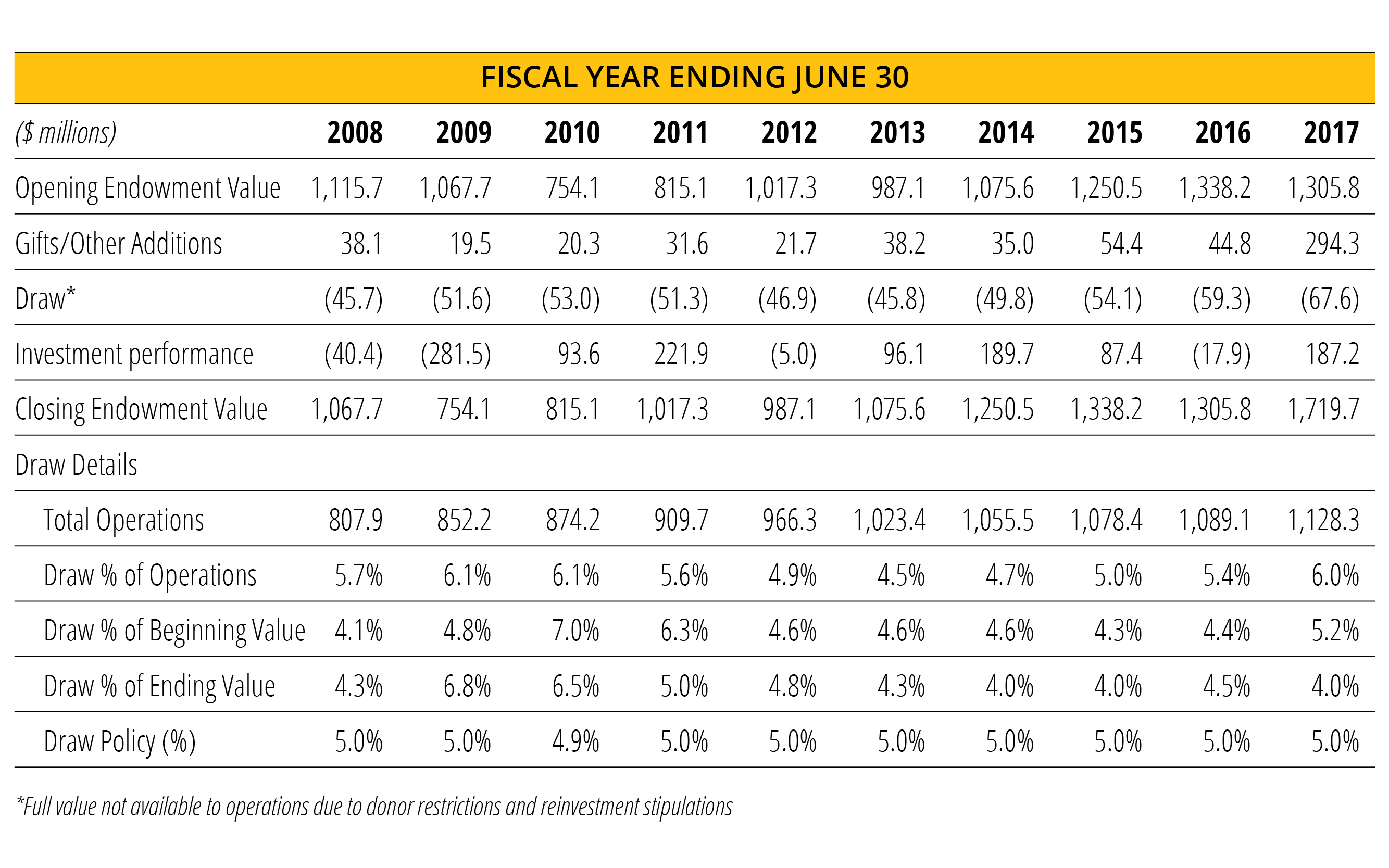

The endowment’s market value increased to $1,719.7 million as of June 30, 2017, from $1,305.8 million as of June 30, 2016. This net increase of approximately $413.9 million reflects the collective impact of $294.3 million from gifts and other sources, $187.2 million from investment gains and $67.6 million of distributions to support the university's operations.

Cash distributions from the endowment (i.e., the draw) provide a key source of support for various university activities and programs ranging from general operations to specific needs, such as scholarships and professorships. As previously pointed out, the endowment remains significantly smaller — both in absolute terms and on a per student basis — relative to our peer institutions, resulting in the operating budget on tuition and private support. The historical activities of the endowment, including the draw and its support expressed as a percentage of annual operations, are summarized in Figure 3.

Figure 3 – Endowment Attribution

During the last decade, the draw from the endowment has contributed, on average, approximately 5.4 percent of the university’s annual operating budget. For fiscal year 2017, the draw from the endowment provided 6.0 percent of the university’s operating budget. Viewed as a percentage of the annual budget, the relative support from the draw is affected not only by the growth in the endowment and the draw formula (see "Note 6" of the consolidated financial statements), but also by the growth in the university’s annual operating budget, which has increased by an average of 3.4 percent annually for the past decade.

The Dietrich Foundation, established by Pittsburgh industrialist and longtime university trustee William S. Dietrich II, was created to manage in perpetuity his gift of approximately $500 million in assets intended to benefit the university and other higher education and charitable institutions. The Dietrich Foundation’s assets are not reflected in the university’s financial statements (see additional information regarding the foundation in Note 16 to the consolidated financial statements). The university’s share of the annual distributions from The Dietrich Foundation is 53.5 percent. If this percentage is applied to the estimated value of The Dietrich Foundation’s assets of $812 million as of June 30, 2017, and the result were added to CMU’s endowment of $1,719.7 million, the combination would total $2,154.1 million. Annual distributions from The Dietrich Foundation over time equal 3.0 percent of the value of The Dietrich Foundation’s net assets as measured on January 1 of each year. The gift for fiscal year 2017 was $12.3 million, and cumulative gifts since the initial gift in fiscal year 2013 have totaled $51.8 million.

With changes designed to enhance the university’s investment program and the continued generosity of the university’s alumni and friends, we are confident that the prospects for long-term growth of endowment assets remain strong — even in the continuing low interest rate environment in which we find ourselves. We believe the university’s investment program — with its long-term focus and global, diversified asset allocation — will enable Carnegie Mellon University’s endowment to continue to strengthen over time, providing greater ongoing support for the university’s operating needs while also preserving purchasing power to support future generations of students, faculty and programs.

Charles A. Kennedy

Chief Investment Officer

October 4, 2017